Legacy’s Guide on Trust Planning and Roth Conversions

How Coordinated Design Can Reduce Multi-Million-Dollar Family Tax Exposure

This guide is designed for families with approximately $5–10 million in total household assets. It explains why trusts and Roth conversions should be planned together, and how doing so can materially reduce lifetime and legacy income taxes.

The Core Planning Opportunity

Under current SECURE Act rules, most non-spouse beneficiaries must withdraw inherited retirement accounts within 10 years. A surviving spouse, however, may stretch distributions over her life expectancy. This spouse lifetime stretch is the single largest tax deferral opportunity in multi-generational planning.

Why Roth Conversions Matter

Without Roth conversions, large traditional IRAs are often inherited by children during their peak earning years, pushing them into the highest tax brackets. Strategic Roth conversions during the spouse’s lifetime can shift taxation to lower brackets, eliminate future bracket compression, and allow assets to pass tax-free to heirs.

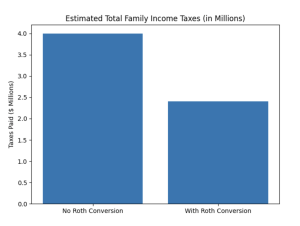

Roth vs. No Roth: Tax Comparison

The chart below illustrates a simplified comparison:

– No Roth Conversion: Approximately $4.0M in total family income taxes

– With Strategic Roth Conversions: Approximately $2.4M in total family income taxes

Although some tax is paid earlier in the Roth scenario, it is paid at lower rates and prevents taxation on decades of future growth. The economic benefit often exceeds $2–3 million for families in this asset range.

Bottom Line

Trusts provide control and protection. Roth conversions change the tax outcome. When coordinated properly during the surviving spouse’s lifetime, families can significantly reduce long-term tax exposure while preserving flexibility and asset protection for the next generation.

This commentary reflects the personal opinions, viewpoints and analyses of the Legacy Trust & Capital Partners employees providing such comments and should not be regarded as a description of advisory services provided by Legacy Trust & Capital Partners or performance returns of any Legacy Trust & Capital Partners client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this commentary constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Legacy Trust & Capital Partners manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.